What is Discounted Cash Flow?

For DCF, see the detailed explanation on pages 330-337 of my book, “The Rules of Super Growth Stocks Investing“, and a step-by-step calculus for a practical example.

Features of this calculator

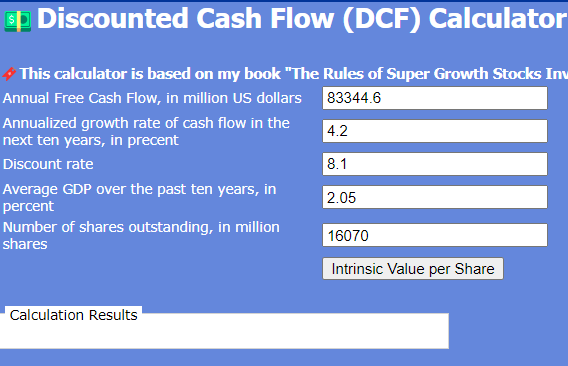

This calculator is used as a calculation template for user to adjust various parameters of the discounted cash flow model according to their own needs and the different company to be calculated, and finally calculate the reasonable intrinsic value of the company.

Please be noted:

- The default value of each field shown on the screen is based on Apple’s data at the end of the second quarter of 2022.

- Clicking on the words “Annual Free Cash Flow” on the screen will open Apple’s important statistics on the Yahoo Finance website, where you can find Apple’s annual free cash flow figures. You only need to change the U.S. stock code of the company on the website to find the statistics of the corresponding company.

- Clicking the words “annualized growth rate of cash flow in the next ten years” on the screen will open the important statistics of Apple on the Yahoo Finance website. You can find Apple’s revenue growth rate in the next few years. This calculates the annualized growth rate of cash flow. You only need to change the U.S. stock code of the company on the website to find the statistics of the corresponding company.

- For the discount rate figures, please refer to the detailed description on pages 330-337 of the book “Super Growth Stock Investing Rules”.

- Clicking on the words “average GDP over the past ten years” on the screen will allow you to query the average GDP and compound growth rate statistics of the United States in the past.

- Clicking on the word “Number of outstanding shares” on the screen will open the important statistics of Apple on the Yahoo Finance website, where you can find the number of outstanding shares of Apple. You only need to change the U.S. stock code of the company on the website to find the statistics of the corresponding company.

How to use this calculator?

Users simply click on this link to connect to the Querier to Annualized rate of return for Taiwan Stock Exchange and see the following screen:

Users only need to input the following fields on the screen:

- Annual Free Cash Flow

- Annualized growth rate of cash flow in the next ten years

- Discount Rate

- Average GDP over the past ten years

- Number of shares outstanding

The default values for the above fields will be based on Apple’s data at the end of the second quarter of 2022. You can change the value of each field of the corresponding company according to the company you want to calculate.

After the input is complete, click the “Intrinsic Value per Share” button on the screen, and you can see the calculation result of the intrinsic value per share in the “Calculation Results” area below.

Two practical examples

In order to let investors understand how to use my free online DCF tool program, you can refer to my following two famous practical examples for step-by-step explanation:

- “What’s TSMC DCF intrinsic value?How to calculate it quickly with a free tool?“: Apply my free online DCF tool program to TSMC and explain it step by step.

- Pages 330 to 337 of my book For DCF, see the detailed explanation on pages 330-337 of my book, “The Rules of Super Growth Stocks Investing“, it use Apple as an example to provide very detailed step-by-step instructions.

Table for US stock investment toolset

Special reminder

For all major market index annualized return query tools listed in the table; including Taiwan Stock Index, Dow Jones Index, S&P 500 Index, Nasdaq Index, Philadelphia Semiconductor Index, not only annualized return query , you can also query the index return rate in any year──just enter the year you want to query in both the start and end fields.

The following is a list of must-have US stock investment free tools developed by Andy Lin:

For the detail, please see “Free online US stock investment toolset".

Buffett’s Reminder on DCF

Terminate value for estimating intrinsic value

Below contents is the full transcript from 1995 Berkshire Hathaway shareholders Q&A meeting.

AUDIENCE MEMBER: — Keith Briar from San Francisco. I have a question. When you’re valuing the companies and you discount back the future earnings that you talk about, how many years out do you generally go? And if you don’t go out a general number of years, how do you arrive at that time period?

WARREN BUFFETT: Well, that’s a very good question. And it’s — I mean, it’s the heart of investing or buying businesses, which we regard as the same thing, but — And it is the framework in which we operate. I mean, we are trying to look at businesses in terms of what kind of cash can they produce, if we’re buying all of them, or will they produce, if we’re buying part of them. And there’s a difference. And then at what discount rate do we bring it back. And I think your question was how far out do we look, and all that.

Despite the fact that we can define that in a very kind of simple and direct equation, you know, we are — we’ve never actually sat down and written out a set of numbers to relate that equation. We do it in our heads, in a way, obviously. I mean, that’s what it’s all about. But there is no piece of paper.

And we never — there never was a piece of paper that shows what our calculation on Helzberg’s or See’s Candy or The Buffalo News was, in that respect. So, it would be attaching a little more scientific quality to our analysis than there really is, if I gave you some gobbledygook about, “Well, we do it for 18 years and stick a terminal value on and do all of this.” We are sitting in the office thinking about that question with each business or each investment. And we have discount rates, in a general way, in mind.

But we really like the decision to be obvious enough to us that it doesn’t require making a detailed calculation. And it’s the framework. But it’s not applied in the sense that we actually fill in all the variables. Is that a fair way of stating it, Charlie?

CHARLIE MUNGER: Yeah. Berkshire is being run the way Thomas Hunt Morgan, the great Nobel laureate, ran the biology department at Caltech. He banned the Friden calculator, which was the computer of that era. And people said, “How can you do this? Every place else in Caltech, we have Friden calculators going everywhere.” And he said, “Well, we’re picking up these great nuggets of gold just by organized common sense, and resources are short, and we’re not going to resort to any damn placer mining as long as we can pick up these major aggregations of gold.”

That’s the way Berkshire works. And I hope the placer mining era will never come. Somebody once subpoenaed our staffing papers on some acquisition. And of course, not only did we not have any staffing papers, we didn’t have any staff. (Laughter and applause)

Discount rate for estimating intrinsic value

Below contents is the full transcript from 1996 Berkshire Hathaway shareholders Q&A meeting.

AUDIENCE MEMBER: Yes. Mr. Buffett, good morning. My name’s Ed Walzak (PH) from New York. I’m a student and an admirer of your investment philosophy. I have a question. In determining a company’s intrinsic value, you seem to write or indicate that you project out a company’s owner earnings for a number of years, and then discount that back by prevailing rates.

My question is, how much of a premium, if any, to prevailing risk-free rates do you demand when you discount back the owner earnings of a company? Or stated differently, for example, today, with loan rates at about 7 percent, if you did the same exercise with Coca-Cola, at what rate of interest would you discount back their owner earnings?

WARREN BUFFETT: Yeah. We get asked that question a lot. And we’ve answered it to some extent in past annual reports about what discount rate to use. We basically think in terms of the long-term government rate. And there may be times, when in a very — because we don’t think we’re any good at predicting interest rates, but probably in times of very — what would seem like very low rates — we might use a little higher rate.

But we don’t put the risk factor in, per se, because essentially, the purity of the idea is that you’re discounting future cash. And it doesn’t make any difference whether cash comes from a risky business or a safe business — so-called safe business. So, the value of the cash delivered by a water company, which is going to be around for a hundred years, is not different than the value of the cash derived from some high-tech company, if any, that — (laughter) — you might be looking at. It may be harder for you to make the estimate. And you may, therefore, want a bigger discount when you get all through with the calculation.

But up to the point where you decide what you’re willing to pay — you may decide you can’t estimate it at all. I mean, that’s what happens with us with most companies. But we believe in using a government bond-type interest rate. We believe in trying to stick with businesses where we think we can see the future reasonably well — you never see it perfectly, obviously — but where we think we have a reasonable handle on it. And we would differentiate to some extent.

We don’t want to go below a certain threshold of understanding. So, we want to stick with businesses we think we understand quite well, and not try to have the whole panoply with all different kinds of risk rates, because, frankly, we think that’d just be playing games with numbers. I mean, we — I don’t think you can stick something — numbers on a highly speculative business, where the whole industry’s going to change in five years, and have it mean anything when you get through. If you say I’m going to stick an extra 6 percent in on the interest rate to allow for the fact — I tend to think that’s kind of nonsense.

I mean, it may look mathematical. But it’s mathematical gibberish in my view. You better just stick with businesses that you can understand, use the government bond rate. And when you can buy them — something you understand well — at a significant discount, then, you should start getting excited. Charlie? (Laughter)

CHARLIE MUNGER: Yeah. The discounts were once greater than we now see.

WARREN BUFFETT: That’s all you’re going to get, folks. (Laughter)

Related articles

- “Andy’s free tools developed for US stock investment“

- “The importance of cash, Apple’s experience in using cash“

- “What’s TSMC DCF intrinsic value?How to calculate it quickly with a free tool?“

- “DCF (Discounted Cash Flow) Calculator“

- “What’s TSMC DCF intrinsic value?How to calculate it quickly with a free tool?“

- “Why is TSMC valuation much lower than US peers?“

- “Investors should care annualized rate of return (IRR), How to calculate?“

Disclaimer

- The content of this site is the author’s personal opinions and is for reference only. I am not responsible for the correctness, opinions, and immediacy of the content and information of the article. Readers must make their own judgments.

- I shall not be liable for any damages or other legal liabilities for the direct or indirect losses caused by the readers’ direct or indirect reliance on and reference to the information on this site, or all the responsibilities arising therefrom, as a result of any investment behavior.