I listed BNPL as one of the future development areas of financial technology in sections 3-5 of my book “The Rules of Super Growth Stocks Investing”. The penetration rate of credit cards is very high, and users have a mature habit of buying first and paying later. However, the user experience is poor, and payment information needs to be entered repeatedly on different websites. With BNPL (Buy now, pay later), you can be automatically identified and enter the payment link when you jump between different independent stations without even logging in. BNPL’s business model is different from traditional credit card companies. The main income does not come from overdue payments from consumers, but from merchants selling goods.

Benefits

Benefits to consumers

The biggest difference from a credit card is that BNPL companies will not charge consumers a fee, but turn to sellers to charge a fee. Consumers can choose to pay in full (Pay Later) or pay in installments (Pay in X) to repay the principal. The former is paid in one lump sum within a certain period of time after the order is placed, and the latter is paid in installments.

As for overdue payments, Block’s Afterpay and Klarna (depending on the situation) will charge overdue payments, but Affirm and PayPal don’t. Generally speaking, overdue payments are still lower than credit cards.

Another big advantage is that BNPL loans will not be included in consumer credit ratings in Europe and the United States (China’s BNPL records will be included starting this week), which is a great advantage compared to credit cards. On the other hand, BNPL’s loan approval review is very fast, because they are all fintech companies, using their own algorithms, and don’t need to wait many days or even a week to get a credit card.

Benefits for merchants

This is because consumers can use this convenient way of consumer lending and can afford to buy more expensive products from manufacturers, which can obviously expand merchants’ business. This is the biggest reason why merchants are willing to be charged (4%-5% vs. credit card 2%). For example, Peloton (ticker: PTON) alone accounted for 30% of Affirm’s total revenue last year! And Block Afterpay’s money collected from merchants accounted for 75.6% of Afterpay revenue.

A survey by Bank of America (ticker: BAC) pointed out that 42% of consumers would use BNPL because of the discounts offered by BNPL companies. A survey by Credit Karma (ticker: INTU) pointed out that 14% of consumers intend to use BNPL to pay for the shopping season at the end of this year.

At present, Amazon (ticker: AMZN) and Shopify (ticker: SHOP), plus Apple (ticker: AAPL) have both joined this battle and cooperated with BNPL companies to provide consumers with a quick and convenient way to purchase and expand their platform transaction volume by the way.

BNPL Companies

BNPL Companies in US and Europe

There are currently four major manufacturers in Europe and the United States. Except for PayPal who joined later and is smaller in scale. According to eMarketer, Klarna, leads this market with a 48.6% share of all the world’s buy-now-pay-later plan users. Then comes Australian-based Block Afterpay with 28.1%. Affirm comes in third with 13.4%.

- Klarna:

- Klarna claim it account for global BNPL 55% GMV share, 250K merchants customers

- In United States, has 20 million users, which is 50% higher than the largest competitor. And 25% of the top 100 retail brands in the US will use Klarna.

- Block Afterpay

- Please refer to my blog’s special article a few days ago, “Why Block (Square) spent heavily to acquire Afterpay“.

- Affirm

- The company went public only this year and was founded by the former chief technology officer of PayPal.

- Has active consumers 5.4 million, and active merchants 12 thousand.

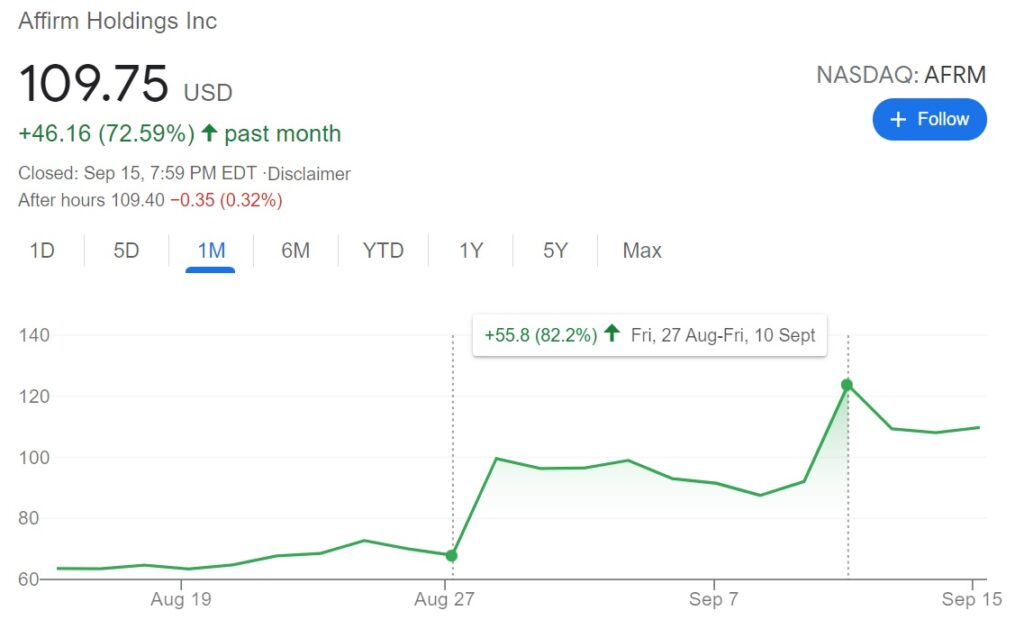

- After announcing the cooperation with Amazon last week, the stock price soared by more than 82% in a few days (as shown in the figure below, from Google Finance).

- PayPal’s Pay in 4

- Last week PayPal acquired Paidy, a well-known Japanese BNPL company.

BNPL Companies in China

The top three BNPL companies in China:

- Huabei, Borrow, and Fabe of Ant Group (parent company ticker: BABA)

- The longest history and the largest market share.

- Huabei cannot withdraw cash, most of which are used for Taobao shopping.

- JieBei borrowing can withdraw cash, most of which are used for larger personal loans, such as decorating houses.

- FaBei is used for employee salary deposit.

- Last year, the ant listing prospectus revealed that there were 500 million of Huabei and JieBei users in Q2 2020 .

- It is the main source of profit for Ant Group, accounting for 39.41% of revenue.

- BaiTiao and JingTiao of JD Digital (parent company ticker: JD)

- According to the content of JD Digital’s prospectus, the scale is about 13-16% of Ant.

- The opponents of BaiTiao and JingTiao are Huabei and JieBei respectively.

- It is the main source of profit of JD Digital, accounting for 43% of revenue.

- Tecent (ticker: TCEHY) FenFu

- There were 240 million users in January this year

However, since China suspended the listing of Ant and JD Digital last year, the future of this business now appears to be full of uncertainties. The general direction that can be determined at present is that technology companies must spin off the financial technology part and return to banking system supervision, but many details are still unclear.

Whose market to grab

Visa also launched similar services such as POS and Pay later to counterattack. Mastercard also has deployed similar services. For details, please refer to the special article on my blog. “Has the moat of the two major credit card network loosened?” .

Conclusion

Some reports point out that the current BNPL market size is US$ 1 trillion, and Block is more optimistic, it estimated market is US$ 10 trillion. BNPL is not whether it will become popular, but it has already been popular in developed countries (including Japan) outside of Taiwan, and it will grow substantially in the next few years. The eMarketer report pointed out that 45 million people in the United States are using BNPL, and 75% of those using BNPL are young people under 40.

Related articles

- “You should know the company Square (rebraned to Block)“

- “Is Afterpay Worth Block (Square) $29 Billion M&A?“

- “The most popular news credit method BNPL“

- “How Sezzle makes money?“

Disclaimer

- The content of this site is the author’s personal opinions and is for reference only. I am not responsible for the correctness, opinions, and immediacy of the content and information of the article. Readers must make their own judgments.

- I shall not be liable for any damages or other legal liabilities for the direct or indirect losses caused by the readers’ direct or indirect reliance on and reference to the information on this site, or all the responsibilities arising therefrom, as a result of any investment behavior.