Company Profile

HP (formerly Hewlett-Packard, US stock code: HPQ) is a giant in the personal computer and printing markets. HP has been focusing on the PC and printing markets since it exited the IT infrastructure business after splitting with Hewlett Packard Enterprise (ticker: HPE) in 2015. HP focuses on the business market but also maintains sales of consumer devices and printers. The company has an extensive global customer base, with only a third of its sales coming from the United States. HP completely outsources production and relies heavily on channel partners for sales and marketing.

Typically a good company, but not a good stock

There is a saying that there are good companies in this world, but the stocks of good companies are not necessarily good stocks. If you can make money for investors as a criterion; HP (Hewlett-Packard, ticker: HPQ) should be one, at least in the past two decades and now. This is what most people think, but is it really so?

There should be few people in the information industry who would deny that HP is a good company, but it may not be profitable to buy its stock, at least for the last twenty years, or for the foreseeable future. I also use it as an example in my 3-1 in my book “The Rules of Super Growth Stocks Investing” to remind readers.

That being the case, what am I going to do with it for discussion? What about the actual situation?

The company was split

In my book “The Rules of Super Growth Stocks Investing”, in order to explain the difference and valuation between personal consumption companies and enterprise companies, I also take HP and Hewlett Packard Enterprise (ticker: HPE) in 3-2 as an example. If HP had not separated from HPE Technology, which is responsible for the enterprise market and servers in the group, in 2015, the company’s market value would have been dragged down. This was the main consideration for the separation at that time.

HP is a typical Silicon Valley company

In fact, everyone is focusing on the other five major technology stocks and software companies because HP has recently gone downhill, but everyone forgets that HP is actually on the same level as Intel. It is a very early predecessor in Silicon Valley. Its head office is still in the center of Silicon Valley. Even in the early days of Hewlett-Packard, it was a large contractor in the US defense industry, and it also made a lot of money because of World War II.

There are many well-known American technologists who are closely related to HP. Apple founder Steve Jobs, when he was twelve years old (I wrote it right, was twelve), volunteered and called HP founder Bill Hewlett and asked him for a job there.

HP split has spawned many famous and important businesses

The following are well-known and important companies spun off from HP, each of which is important:

- Hewlett Packard Enterprise (US: HPE): 2015 split

- Agilent Technologies (Agilent Technologies, ticker: A): 1999 split

- Avago (Avago, ticker: AVGO): 1999 split. Please refer to my post “Significant changes in Broadcom’s business approach“

HP has acquired many famous companies

The following are notable and important companies that HP has acquired, each of which is important:

- Broadcom, 2016 Avago Technologies acquires Broadcom. Please refer to my post Hewlett Packard Enterprise (ticker: HPE): 2015 split

- Agilent Technologies (Agilent Technologies, ticker: A): 1999 split

- Avago (Avago, ticker: AVGO): 1999 split. Please refer to my post “Significant changes in Broadcom’s business approach“

- Autonomy, 2011 M&A, this M&A has caused great harm, causing HP to be miserable, and indirectly causing the spin-off of HP and HPE Technology

- 3Com, 2010 M&A

- Palm, 2010 M&A

- EDS, a merger in 2008, spent $13.9 billion, which caused a stir in the technology world at the time.

- Aruba, 2001 M&A

- Compaq, acquired in 2001; forms the main body of what you see now as HP.

- The consulting arm of PwC, which was acquired in 2000, spent $18 billion, and now doesn’t seem to be very successful.

- Digital (DEC), which was acquired by Compaq Computer in 1998

- Verifone, acquired in 1997

- Computer division of Texas Instruments, acquired in 1992. Please refer to my post “Good companies are rare, two or three will make you very rich“

- Apollo Computer, acquired in 1989

HP is closely related to the entire electronics industry

In particular, notebook computers, electronic foundries, and Taiwan’s electronic industry are almost inseparable from HP. I can’t think of an electronics foundry in Taiwan. HP is not one of its major customers. Its biggest competitor Dell’s current internal operating and engineering model is almost a copy of HP (two decades ago, the two were very different, because the business and scale of the two were so different then, and now they are almost the same).

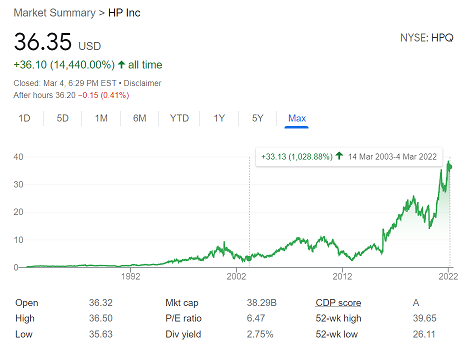

Market valuation

| As of 3/2/2022 | Numbers |

| Stock price | 36.31 |

| Market capitalization | 38.25 billion |

| P/E | 6.46 |

| Dividend yield | 2.75% |

| Stock performance in past year | +21.76% |

Note that HP is a blue-chip blue chip stock, which is one of the reasons why it pays a high dividend. The dividend yield is 2.75%, which is very high in the US stock market. Its price-earnings ratio is only 6.46, and its shares have risen 21.76% over the past year (please note this, due to the assistance of the COVID-19 panemic).

2021 performance

| FY2021 | Annual Growth | |

| GAAP net revenue ($B) | 63.5 | 12.1% |

| GAAP operating margin | 8.4% | 6.1% |

| GAAP net earnings1 ($B) | 6.5 | 129% |

| Free cash flow ($B) | 4.2 | 3.9% |

This kind of performance still looks like a blue-chip company. It is quite satisfactory and will not have too many bright spots. It is suitable for conservative investors to hold. However, investors should be reminded that the revenue growth in 2021 can be 12.1%, which is a great growth for a PC COVID-19 pandemic. The real test will be this year after the pandemic.

Stock performance in past 2 decades

Its stock price has risen by 1028.88% in the past 20 years! (Intel was only 117.4% in the same period) After the split of HP and HPE Technology in 2015, it rose 366%. It is clear that most of its rise has occurred in the past few years, especially during the pandemic. Students who fail the test every time, suddenly become good students, of course the stock price does not perform badly. In the second quarter of 2019, it has risen by 77% so far, which is a good performance among blue-chip companies that have been established for more than 50 years.

Intel should have had the worst share price performance over the past 20 years among the large-cap stocks I am familiar with (all I know, not just tech). The performance of 117.4% is less than 1/4 of that of the S&P 500 during the same period, and the past 10 years have been a rare bull market for US stocks.

Let’s compare the performance of Intel (ticker: INTC) during the same period, at least HP beat Intel in every period.

Closing words

Investing in HP doesn’t look like you’ll make a lot of money right now, but it’s still a blue-chip business if you invest for the long term; at least you won’t lose your capital in the long run, and you’ll get a dividend. Many people may think that as the PC goes out of business, it goes out of business and stock becomes wallpaper, which should be overkill. The capital market in the United States is very active, and HP still has a lot of invisible and valuable assets. HP still has a lot of invisible and valuable assets, or why Xerox (ticker: XRX) and various private equity companies are drooling and want to acquire it.

If you want to know more about this famous company, you can read “The HP Way” by one of the HP founder David Packard. A wonderfully written book that still impresses me to this day.

Related articles

- “Seagate comeback thanks to AI, No 1 S&P 500 perform stocks YTD“

- “How does HP make money? The pros and cons of investing in HP“

- “Ticker symbol changed companies’ stock performance?“

- “HPE expertizes on enterprise technology services“

- “How does the resurrected Dell make money?“

- “AI PC is changing the PC supply chain and ecosystem“

- “Supermicro, a repeat offender of scandals, valuation is not justified and unsustanable, no worth for long-term holding“

- “How does IBM make money? What’s next?“

- “Is Buffett no longer hold for long haul? TSMC, HP, and US Bancorp cases study“

- “How does Texas Instruments make money? Amazing long term capital reward and company net profit margin!“

Disclaimer

- The content of this site is the author’s personal opinions and is for reference only. I am not responsible for the correctness, opinions, and immediacy of the content and information of the article. Readers must make their own judgments.

- I shall not be liable for any damages or other legal liabilities for the direct or indirect losses caused by the readers’ direct or indirect reliance on and reference to the information on this site, or all the responsibilities arising therefrom, as a result of any investment behavior.