Company Profile

company’s history

Charles Liang , the founder and CEO of Super Micro Computer or Supermicro (ticker: SMCI), graduated from the Department of Electrical Engineering of the National Taiwan University of Science and Technology and received a master’s degree from the University of Texas.

Supermicro was founded by Charles Liang in 1993. It started with only five people, all Charles Liang’s brothers or relatives, run by Charles Liang and his wife and company treasurer Chiu-Chu Liu.

A manufacturing subsidiary, Ablecom, was opened in Taiwan in 1996 and in the Netherlands in 1998.

IPO

On March 8, 2007, Supermicro went public in the United States.

Main products

The company’s main products include server hosts, storage, motherboards, cabinet solutions, network devices, server management software, workstations, etc. Its customers include data centers, cloud computing, enterprise information technology, big data, high-performance computing, super Computers, embedded systems, etc.

A Taiwanese company

Supermicro’s company is registered in the United States, but most of the company’s production, research and development, and shipping focus are in Taiwan. The company also has an office in Taoyuan, Taiwan.

Operating performance

Performance in the fourth quarter of 2023

In the company’s annual report for fiscal year 2023, CEO Charles Liang said that the continued growth of artificial intelligence computing may have a greater impact on the world than the industrial revolution more than 200 years ago. His company is indeed growing like this.

Supermicro reported record revenue of $3.66 billion for the fourth quarter ended December 31, 2023, an annual increase of 103%. Adjusted earnings per share were $5.59, up from $3.26 in the same period in 2022. Annualized adjusted earnings per share are $22.36, with a forward price-to-earnings ratio of 25.9.

Reasons for the revenue surge

The company continues to benefit from demand for Nvidia’s (ticker: NVDA ) graphics processing units (GPUs), so it’s driving higher sales of Supermicro’s AI rack systems as supply of these chips increases.

2024 Operating Outlook

Charles Liang said in his 2023 annual letter to shareholders: Management expects revenue to double in fiscal 2024, reaching a range of US$14.3 billion to US$14.7 billion. “With the booming development of artificial intelligence applications, it is expected that the annual revenue target of US$20 billion will be achieved within a few years.”

Capital market performance

Stunning share price performance

In 2023, the stock price of Super Micro (ticker: SMCI) increased by 238.97%. From 2024 to the end of February, it has increased by 203.42%; the stock price has soared by more than 825% in the past year. The market value has exceeded US$50 billion.

March 2, 2024, S&P Dow Jones Indices announced that Super Micro has been included as a component stock of the S&P 500 Index for the first time.

Fragile Valuation

Supermicro has a forward price-to-earnings ratio of 25.9, putting its valuation in line with International Business Machines Corp. (ticker: IBM ). This is odd because IBM is a larger, more productive company that sells software and consulting services in addition to hardware.

Wall Street’s expectations for Supermicro’s stock price vary widely. The consensus price of $652 shows that Supermicro stock is currently overvalued──by a lot. There are certainly investment banks that have set a price target of $1,300 — showing the fragility of Supermicro’s valuation.

Share price comparision

| Company name | Ticer | Share price | 2023 share performance | YTD share performance | P/E |

| Supermicro | SMCI | 1163 | 246.24% | 307.43% | 90.9 |

| Dell | DELL | 113.55 | 90.20% | 51.83% | 26.04 |

| HP Enterprise | HPE | 18.05 | 6.39% | 6.62% | 12.42 |

| Lenovo | LNVGY | 24.53 | 72.76% | -12.05% | 17.5 |

| IBM | IBM | 197.78 | 16.08% | 22.46% | 24.58 |

| Nvidia | NVDA | 919.13 | 238.87% | 90.82% | 77.03 |

| AMD | AMD | 202.76 | 127.59% | 46.31% | 385.81 |

| Intel | INTC | 45.24 | 90.12% | -5.36% | 112.82 |

| S&P 500 index | 5,175.27 | 24.23% | 9.12% | 23.27 |

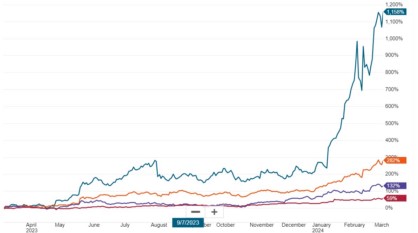

In Figure 1 below, the lines from top to bottom respectively represent the comparison chart of the stock price trends of Supermicro (1158%), Nvidia (282%), AMD (132%), and IBM (59%) over the past year. Obviously, in mid-January 2024, Supermicro’s stock price showed a trend of climbing from the ground up.

Figure 1: Comparison of stock price charts of Supermicro and related companies over the past year (Graphic from Charles Schwab)

Why it is not worth chasing

Choked by someone

In a word, Supermicro has absolutely no autonomy in its business. It is a typical manufacturer that relies on others, that is, it can be choked by others at any time──Intel (ticker: INTC), Nvidia and AMD (ticker:AMD) If the three major chip manufacturers find a manufacturer with higher cooperation and lower assembly prices, they may be in trouble at any time.

Nvidia recently revealed supply difficulties in its supply chain – a problem that has existed for quite some time. This issue has the potential to have a domino effect on Supermicro.

Supermicro’s other strong relationship is with Nvidia’s top competitor Advanced Micro Devices. After Supermicro reported mixed fourth-quarter 2023 earnings earlier in 2024, some investors had legitimate concerns about Supermicro’s long-term growth prospects. Likewise, if demand for AI chips stagnates, both Nvidia and AMD will be affected, which will affect Supermicro.

No moat

Many people will argue that Supermicro is famous for its liquid cooling technology for high-power semiconductors, but there is no so-called moat for liquid cooling, a heat dissipation technology.

Supermicro’s main business is a server assembler. To put it bluntly, it buys server chips and electronic components, assembles them, and ships them under its own brand. This business model is the same as that of Taiwan’s electronics OEMs. The difference is that Supermicro has its own brand.

But the problem is that there is no moat in the business model of server assembly, especially for smaller manufacturers like Supermicro. Without software, additional services, and channel integration capabilities, it is difficult to compete with the giants in the industry. compete.

Growth is unsustainable

Supermicro’s current astonishing stock price and valuation levels are mainly based on a three-digit percentage annual revenue growth rate, but the problem is that this three-digit percentage annual revenue growth rate is not sustainable.

If demand for AI servers begins to wane, AMD’s profitability could experience a more significant decline.

Whether a company is sustainable or not is extremely important. For this part, please see the explanation of my article below:

- “Sustainability matters in stock market investing“

- Sections 2-3 of my book “The Rules of 10 Baggers“, “Most of the good performance of 10 bagger stocks is sustainable”, pages 94-97

- In sections 1-2 of my book “The Rules of Super Growth Stocks Investing“, page 30, there are three reasons for the rise in stock prices: the first of which is 1. The continued growth of corporate earnings. In section 2-1, pages 78-83, I am selecting three filtering criteria that companies with strong competitive advantages must pass: Among them, criterion 2》Is the company’s profits sustainable? In section 6-1, page 274, how do we sift through a bunch of companies that seem to have potential and identify companies that are more likely to become 10x shares in the future?

Ultra-low profit margin industry

The company is actually a low-margin enterprise. In the fourth quarter of 2023, which ended on December 31, 2023, Supermicro reported a gross profit margin of only 15.4%. In comparison, gross profit margin for the same period in 2022 was 18.7%.

In 3-1 of my book “The Rules of Super Growth Stocks Investing“, I take Hewlett-Packard (ticker: HPQ) and Hewlett Packard Enterprise (ticker: HPE) as examples. 3-1 also specifically lists a series of industries to remind long-term investors not to touch.

Competitors are too powerful

Supermicro’s main competitors include IBM, Dell (ticker: DELL), HPE, Inspur, Lenovo, and Huawei. These competing manufacturers are not weaklings. Each of them has been a dominant player in the market for decades and has diversified services and networks. Unlike Supermicro, which only engages in server assembly, a business without a moat.

Please note that servers are faced by large enterprises, especially very large enterprises. Hardware price is usually not the only factor in the final decision. Enterprises need complex and diversified services. This is the fatal point of Supermicro. In the long term, survivability is in doubt.

Reasons not recommended to hold

Valuation is unreasonable and unstainable

Supermicro’s biggest problem is that its current valuation is inconsistent with management’s long-term goal of forecasting annual revenue of $25 billion. In the first quarter of 2024, Supermicro reported a profit margin of 10% and it will generate annual profits of $2.5 billion. Supermicro currently has a market capitalization of $48 billion, so if all these predictions are true, it would trade at a price-to-earnings ratio of about 19 times. However, it currently has a P/E ratio of 44.8 and a forward P/E ratio of 22.

Given Nvidia’s current forward price-to-earnings ratio is only 34 times. It is reasonable that Supermicro’s valuation should be much lower than Nvidia’s, because it does not have Nvidia’s moat and is just one of Nvidia’s many suppliers. In reality, Supermicro is not have that much differentiating technology or profit levels.

Repeatedly involved in negative scandals

Another reason is that the company’s “repeated” involvement in negative scandals will affect the company’s credibility. There is a well-known saying on Wall Street: “Don’t touch companies that are riddled with lawsuits, involved in legal cases, or have negative scandals.”

Buffett said, “If you find a cockroach in the kitchen, there will definitely not be one cockroach”, In 1989 Berkshire Hathaway shareholders letter, he wrote “beware of companies displaying weak accounting. If a company still does not expense options, or if its pension assumptions are fanciful, watch out. When managements take the low road in aspects that are visible, it is likely they are following a similar path behind the scenes. There is seldom just one cockroach in the kitchen.”

For Supermicro’s notorious scandals history, please read my post of “Supermicro Founder smuggling cast doubt future“

Lessons from the past

Buffett invests in HP

I’m not exaggerating. When Buffett made a big bet on HP, I personally thought it would be a failed investment at the time. There are many reasons, including:

- The technology industry is outside his circle of competence.

- A good company is not necessarily a good stock; HP is a good company, but not a good stock. HP meets Buffett’s stock selection criteria in many aspects (for details, see the analysis in my other post “The commonalities of Buffett portfolio – cheap, fixed income, repurchase“), which is why Buffett will invest in it. s reason.

- When Buffett invested, HP happened to be working from home due to the epidemic, resulting in a surge in demand for notebook computers. The resulting revenue performance was simply unsustainable (this is the key point, please see what I repeatedly said in the section “Growth is Unsustainable” earlier in this article.)──Because the global PC shipment growth rate in the past two decades has been single-digit percentages. Sure enough, in 2022 after the epidemic was lifted, global PC shipments fell by 16.2%, see notes below.

- Laptop computers are euphemistically called a technology industry, but they are actually a sunset industry, not very different from the manufacturing of televisions.

- As mentioned before, in 3-1 of my book”The Rules of Super Growth Stocks Investing“, I took Hewlett-Packard as an example. For the reasons listed, I specifically used HP as an example in the book.

Note: Gartne’s report states that global personal computer shipments fell by 16.2% in 2022, the largest decline since the agency began tracking this data in the mid-1990s. Full-year personal computer shipments were only 286 million units.

The result

On April 6, 2022, it was first revealed that Buffett had purchased HP, buying nearly 121 million HP shares, accounting for about 11.4% of HP’s equity. At that time, it also inspired HP to surge by about 10% after the market opened.

It began to accept losses on September 13, 2023, and reduced its holdings of HP stocks along the way.

As of November 30, 2023, Buffett’s company has significantly reduced its holdings in HP by 47.37%. HP’s shareholding ratio in Berkshire has dropped to 0.48%, and its total holdings have also dropped to 5.20% of HP’s issued shares.

Nothing is different this time

Templeton once said a famous saying in the investment community, “This time it’s different. These are the four most expensive words in the English language.”

Most of the investors who made crazy bets on shipping stocks in 2020 suffered heavy losses, and this was only three years ago!

Negative news is part of investing; but most investors don’t want to hear the truth.

I am the author of the original text, the essence of this story was originally featured on Smart Magazine, Issue of April 2024

Related articles

- “Supermicro Founder smuggling cast doubt future“

- “Supermicro, a repeat offender of scandals, valuation is not justified and unsustanable, no worth for long-term holding“

- “Seagate comeback thanks to AI, No 1 S&P 500 perform stocks YTD“

- “How GPU farms CoreWeave make money?“

- “How does Applied Digital make money?“

- “DeepSeek routed the global AI and stock“

- “Chinese AI progress and top companies“

- “How Vertiv, share price return 2.5 times of Nvidia, make money?“

- “AI PC is changing the PC supply chain and ecosystem“

- “Artificial intelligence benefits industries“

- “Why did US largest electricity Vistra, a turned around company, share return higher than Nvidia?“

- “How does the resurrected Dell make money?“

- “HPE expertizes on enterprise technology services“

- “Is Buffett no longer hold for long haul? TSMC, HP, and US Bancorp cases study“

- “The commonalities of Buffett portfolio – cheap, fixed income, repurchase“

- “How does HP make money? The pros and cons of investing in HP“

- “How does IBM make money? What’s next?“

- “Negative message is part of investment“

- “Why did US largest electricity Vistra, a turned around company, share return higher than Nvidia?“

- “A investor can be sustained or not? how to verify?“

- “Sustainability matters in stock market investing“

- “The reasons for Nvidia’s monopoly and the challenges it faces“

- “How does the all-powerful Huawei make money?“

- “Major artificial intelligence companies in US stocks market“

- “The artificial intelligence bubble in the capital market is forming“

- “How does nVidia make money, Nvidia is changing the gaming rules“

- “Why nVidia failed to acquire ARM?“

- “Revisiting Nvidia: The Absolute Leader in Artificial Intelligence, Data Center, and Graphics“

- “Data center, a rapidly growing semiconductor field“

- “OpenAI, the Generative Artificial Intelligence rising star and ChatGPT“

- “Artificial intelligence investment trap“

- “Will Intel go bankrupt?“

- “How does Intel make money? and the benefits to invest in it“

- “Intel’s current difficult dilemma“

- “How AMD makes money? A rare case of turning defeat into victory“

- “Why is AMD’s performance so jaw-dropping?“

Disclaimer

- The content of this site is the author’s personal opinions and is for reference only. I am not responsible for the correctness, opinions, and immediacy of the content and information of the article. Readers must make their own judgments.

- I shall not be liable for any damages or other legal liabilities for the direct or indirect losses caused by the readers’ direct or indirect reliance on and reference to the information on this site, or all the responsibilities arising therefrom, as a result of any investment behavior.